Modelling equity market term structures

Abstract

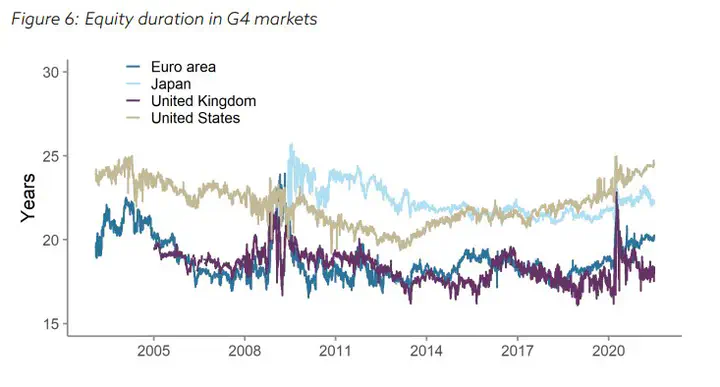

We outline a present-value modelling approach for estimating term structures of expected dividend growth and risk premiums in equity markets. We apply our methodology to equity markets in the US, euro area, Japan and UK.

Publication

NBIM Discussion Note